More than 42 million U.S. households (nearly one-third of the nation) are cost-burdened, paying over 30 percent of their income on housing. Half are renters. In 2023, 22.6 million renter households were cost-burdened and 12.1 million severely cost-burdened, paying more than half their income on rent.¹

The supply story is equally out of balance. Multifamily completions surged to roughly 600,000 in 2024, the highest since the late 1980s, briefly easing rents. But new starts have fallen sharply.² As this surge is absorbed and today’s weak starts catch up, deliveries will collapse by 2025–26, tightening vacancy and pushing rents higher again.³

Meanwhile, what does get built increasingly misses the market most people can afford. Developers face an impossible equation: regulatory costs add about 40 percent to every new apartment,⁴ permitting can take years (San Francisco averages 627 days⁵, and construction costs have risen roughly 20 percent in five years.⁶) High interest rates and the recent flood of supply further squeeze margins. The result is that new ground-up projects often can’t pencil at rents the majority of renters can pay.

This creates a bifurcated rental market. Luxury buildings compete for a small pool of high-income tenants, while wages for everyone else lag inflation and rent growth. Market-clearing rents keep creeping upward, leaving millions priced out. To keep a roof overhead, many renters are forced to move farther away, accept substandard conditions, live with roommates, or devote an ever-larger share of their paycheck to rent; crowding out savings and wealth-building.

The math is clear: ground-up development is expensive, risky, and too slow to meet today’s need for lower-rent housing. We need a way to add supply at rents people can actually afford, something that may seem counterintuitive within the current development model but is entirely possible if we think outside the box. One such opportunity lies hidden in plain sight: the thousands of underused hotels in almost every U.S. market.

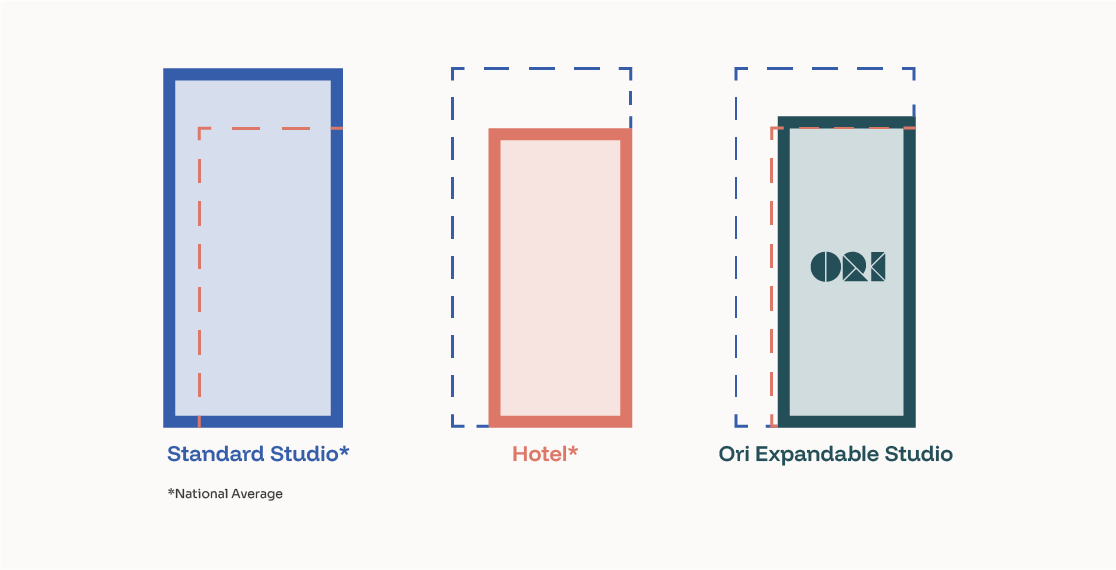

Hotels were built to house people. Typical rooms (250–350 square feet) fall just below national average studio sizes. Core systems like plumbing stacks, elevators, and life-safety are already in place. Unlike office conversions, which wrestle with deep, dark floorplates, hotels are optimized for light and circulation. Hotels face the opposite challenge: shallow floorplates.

Here’s the blunt truth: hotels are hurting. Many never fully recovered from the pandemic. Occupancy collapsed to ~40% in 2020.⁹ As of mid-2025, distress remains widespread:

For multifamily developers, this is an opportunity hiding in plain sight. Low acquisition costs and existing infrastructure mean lower per-unit bases, faster cash flow, and stronger IRRs.

Adaptive reuse isn’t just financially efficient: it’s politically popular. Conversions can qualify for historic tax credits, abatements, and adaptive-reuse incentives.⁸ Cities like them because they deliver housing without lengthy rezoning battles, they align with the push for more “missing middle” housing, and may serve as a missing link in the chain toward naturally occurring affordable housing.

Sustainability is another accelerant. Reuse avoids demolition waste, reduces embodied carbon, and appeals to ESG-driven investors. Renters care too: eco-conscious tenants increasingly choose buildings that reflect their values, boosting occupancy and NOI.

And don’t forget the NIMBY factor: conversions don’t add new shadows or height. They simply repurpose already-accepted buildings, breathe in new life, and strengthen the community with more permanent residents.

If hotel-to-housing conversions are such a no-brainer, why haven’t we seen more? Because past efforts often failed on livability. Many targeted Class C properties (older buildings in less desirable locations with deferred maintenance and underused amenity spaces) simply rebranded hotel rooms as apartments without confronting their limited size or designing for everyday life.

Developers rarely provided creative ways to make small spaces feel spacious. Few offered integrated storage, updated MEP building systems, or flexible layouts to solve it. Instead, they relied on low-cost finishes and static floor plans that left residents with awkward, hard-to-furnish rooms. In many cases, oversized amenity spaces were meant to compensate, but gyms and lounges cannot fix a cramped kitchen, lack of natural light, or a unit that is not designed for permenant residency.

The result was predictable: units that struggled to lease, attracted short-term tenants, and turned over frequently. Many of these early conversions remain stuck at the lower end of the market, underperforming financially and reinforcing the perception that hotel-to-housing doesn’t work. What failed wasn’t the concept of conversion itself; it was the absence of design and the necessary solutions that could transform small footprints into homes people genuinely want to live in.

Ori Expandable Apartments solve the design challenge that has held many hotel conversions back. Instead of tearing down walls or reconfiguring floorplates, Ori hardware transforms compact hotel rooms into functional, stylish apartments. Beds disappear. Workstations and extra storage glide out. Walls move. Rooms shift effortlessly from day to night.

By making a 250 sf room feel like 400 sf or more, Ori delivers livability that outperforms conventional layouts. In Arlington, Ori units were 29 % smaller but rented for only 6.5 % less, commanding a 32 % rent-per-square-foot premium. In Tampa, units were 33 % smaller and rented for just 7 % less, generating a 40 % premium.¹³ The result is apartments up to 40 % smaller that don’t compromise on livability and rent for only about 10 % less. Renters get aspirational living without sacrifice. Developers get stronger NOI and lower costs. Cities get more attainable housing faster.

Ori’s approach aims higher, lifting properties toward the border of Class A and B. By focusing on interiors that are multi-functional, effortless, and magical, we create homes that feel premium while staying attainable. This elevates renter appeal, strengthens absorption and retention, and improves development spreads, making the entire project more desirable and financially resilient.

Unlike the amenity arms race that fuels luxury competition and widens the gap between high-end buildings and the rest of the market, Ori puts the value where it belongs: inside the unit, where residents actually live every day.

Conversions don’t just benefit developers and renters; they lift neighborhoods. Empty hotels drag down local economies. Converted apartments restore foot traffic, support small businesses, and stabilize property values.

Hotels are also often in walkable, transit-rich neighborhoods. That matters: 79% of Americans say walkability is important, and 78% are willing to pay more for it.¹⁴ Homes in walkable neighborhoods sell for ~23.5% more.¹⁵ Whether the goal is to capture that added value or to channel it toward greater affordability, the pattern is clear.

We won’t solve the housing crisis with ground-up construction alone. Distressed hotels are centrally located, underused, and convertible now.

Ori makes that transformation effortless. By turning compact hotel rooms into expandable apartments, Ori unlocks value where others see limitation. Projects pencil. Renters thrive. Cities benefit.

Whether you’re already pursuing hotel-to-multifamily conversions or just starting to explore what you may have overlooked, Ori is here to help make them not only possible but profitable. Let’s turn vacancies into vibrancy together.

1. Harvard JCHS, America’s Rental Housing 2024.

2. NAHB analysis of Census Bureau housing completions, 2024.

3. Federal Reserve Bank of Richmond, “Multifamily Construction in 2024.”

4. NAHB/NMHC, “Regulation: 40.6% of Multifamily Development Costs” (2018).

5. San Francisco Chronicle, “Why SF Permitting Takes 627 Days,” 2023.

6. ENR Construction Cost Index (2019–2024 trend).

7. Associated Builders & Contractors, Construction Workforce Shortfall 2025.

8. National Trust for Historic Preservation, “Federal Historic Tax Credit Overview.”

9. STR, U.S. Hotel Performance, 2020.

10. Trepp, CMBS Special Servicing Report, July 2025.

11. CBRE, U.S. Hotel Trends 2025; AHLA Cost Trends.

12. SF Standard, “Hilton Union Square & Parc 55 Sale at 65% Below 2016 Values,” July 2025.

13. Ori internal case studies, Arlington (2023), Tampa (2024).

14. National Association of Realtors, Community & Transportation Preferences Survey, 2023.

15. Redfin/Walk Score, “The Value of Walkability,” 2022.

16. CoStar, “Chicago Holiday Inn Sells at a Discount to Debt Owed,” (2024)

17. Connect CRE, “250-Room Virgin Hotels Chicago Sold at Discount,” (2025)

Ori Design Studio

Brooklyn, NY