Imagine if airlines still sold tickets with only two choices: coach or first class. Or if Netflix offered just one subscription tier. The fewer price points you have, the more value you leave on the table. Economists call this price discrimination: the idea that the more ways you segment your product, the more of the market’s willingness to pay you can capture.

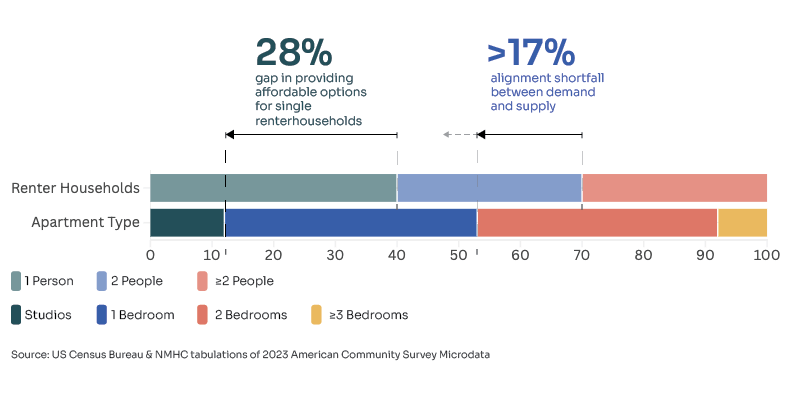

Multifamily housing is no different. For decades, developers have leaned on a familiar unit mix convention, roughly 60% one-bedrooms, 30% two-bedrooms, 10% studios. This approach, while not codified as law, became industry shorthand: a safe template lenders accepted and developers replicated. But if the goal is to maximize revenue, relevance and market demand, the old segmentation model doesn’t go far enough.

In economics, pricing strategy evolves along three primary stages:

Multifamily housing mostly lives in the middle stage of segmentation. A handful of unit types create a few tiers of pricing with occasional overlap depending on the market. The closer developers move toward more pricing options, the closer they get to maximizing yield. In other words: the more price points you offer, the more value you capture.

The 60-30-10 convention emerged because it was rational for its time. One-bedrooms offered predictable demand, two-bedrooms appealed to sharers and families, and studios were capped at a small share that lenders saw as prudent. The practice was driven chiefly by risk avoidance rather than by maximizing returns or serving buyers optimally.

Developers weren’t wrong to adopt this formula. For decades, it penciled. It was legible to lenders, familiar to appraisers, and backed by precedent. In today’s market, the conditions that made this convention safe have shifted, and what once was prudent now risks leaving opportunity untapped.

Today’s housing realities look very different from when the 60-30-10 convention spread. Several pressures expose its limitations:

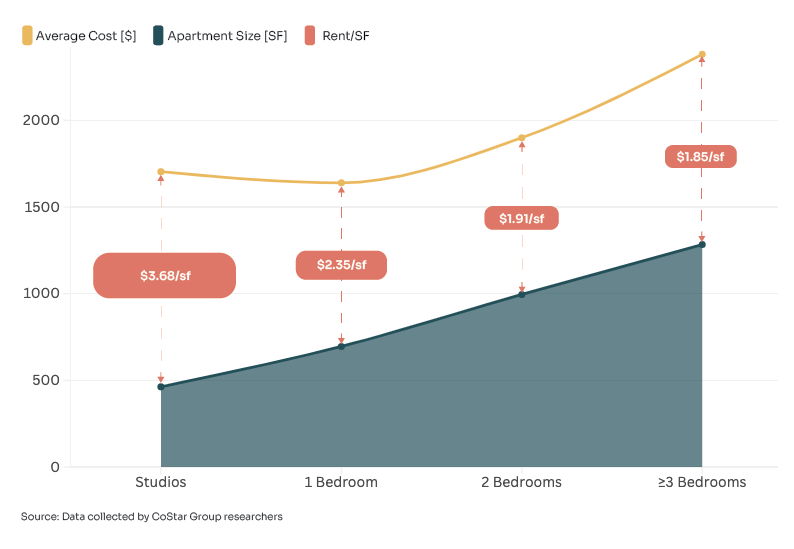

Together, these forces mean that the old segmentation model, with its narrow range of unit types, underserves demand and constrains revenue capture. The data tell the same story: while apartments keep getting smaller, costs keep climbing, and rent per square foot keeps rising.

Think back to airlines: when economy plus, premium economy, and business class entered the picture, airlines didn’t just add seats: they added price points. The result was higher total revenue without alienating budget travelers.

The same principle applies in multifamily. By introducing more small, livable unit types, developers add rungs to the pricing ladder. Instead of losing renters who can’t afford a one-bedroom, you capture them with an aspirational studio. Instead of flattening rents across a narrow mix, you widen the funnel of demand and pull more value from the market.

Case in point: In Arlington, Ori-equipped studios were 29% smaller yet achieved a 32% rent-per-square-foot premium. In Tampa, Ori units 33% smaller captured a 40% $/SF premium. More price points meant faster absorption, higher NOI, and stronger overall asset performance.

Ori sees a clear opening: lean more heavily on smaller, high-performance homes without abandoning one- and two-bedrooms. The goal is a smarter balance that meets renter demand and strengthens asset economics.

By making compact units both desirable and profitable, Ori enables developers to add more studios and smaller one-bedrooms without compromising livability, renter satisfaction, or asset performance.

Traditionally, smaller units meant steeper discounts because they compromised livability. Micro-units became shorthand for cramped, uninspiring spaces. Ori flips that equation.

With Ori, apartments can be up to 40% smaller but feel expansive. Beds vanish, walls glide, rooms expand all with a touch. Renters pay about 10% less in monthly rent, but developers capture 30–40% higher rent per square foot, with NOI gains of up to 50%.

In practice, Ori-enabled buildings lease faster. In Arlington, Ori units stabilized months ahead of conventional comparable units. In Tampa, they were the only units in the building that didn’t require concessions. Smaller didn’t mean compromised. Proof that design, not square footage, defines desirability.

Expanding the pricing spectrum isn’t just good economics for one building. It reshapes feasibility across entire markets.

This isn’t about packing people tighter. It’s about matching homes to how people live today and unlocking projects that are both livable and financially viable.

The old unit mix convention was never wrong. It was a smart hedge for its time. But today, clinging to it is like running an airline with only coach and first class. You’re leaving money and demand uncaptured.

Economics shows a simple truth: a wider range of price points creates more total value, capturing returns for developers while meeting more household needs. Perfect price discrimination may be theoretical, but Ori moves multifamily closer by expanding the spectrum of unit options without shrinking the renter experience.

For developers, this means faster lease-ups, stronger NOI, and new sites brought into play. For renters, it means attainable homes that feel expansive, not compromised. And for cities, it means more housing supply delivered where it’s needed most.

The next era of multifamily will not be built on narrow conventions. It will be built on intentional design, broader price points, and aspirational, expandable living.

1. U.S. Census Bureau, "American CommunitySurvey" (2023)

2. JCHS, "State of the Nation 2025", (2025)

3. NAHB, “Cost to Construct a Home Rose Significantly Over Last Two Years” (2025)

4. RentCafe, “Average Apartment Size in U.S. Increases” (2025)

5. U.S. Census Bureau, “Nearly Half of Renter Households Are Cost-Burdened” (2024)

6. U.S. Census Bureau, “Survey of Market Absorption” (2025)

7. RentCafe, “Average Apartment Size Goes Down in 2022” (2023)

8. RentCafe, “US Average Apartment Sizes” (2025)

9. Apartments.com, “Rent Trends in the United States” (2025)

10. NCHFA, “Construction Cost Increases and the Impact on Housing Affordabilit,”(2024)

11. Construction Drive, “5 years after COVID hit, contractors still wait for prices to come down” (2025)

12. Fortune, “Rent is so expensive for Gen Zers that almost one-third are living with their parents” (2024)

13. Amenify, “Investment Insights: Overcoming Rental Market Hurdles” (2025)

14. Morris & Garritano, “Rising Material Costs in the Construction Industry and How it Affects Insurance Rates” (2024)

15. NAR, “2023 Community and Transportation Preferences Survey” (2023)

16. Urban Institute, “Small Apartment Buildings Can Help Address Housing Shortages, but High Land Costs and Interest Rates Are Limiting Construction” (2025)

17. US Government Accountability Office, GAO, “The Affordable Housing Crisis Grows While Efforts to Increase Supply Fall Short” (2023)

18. Brookings Institute, “Making apartments more affordable starts with understanding the costs of building them” (2020)

Ori Design Studio

Brooklyn, NY